8/19/2024

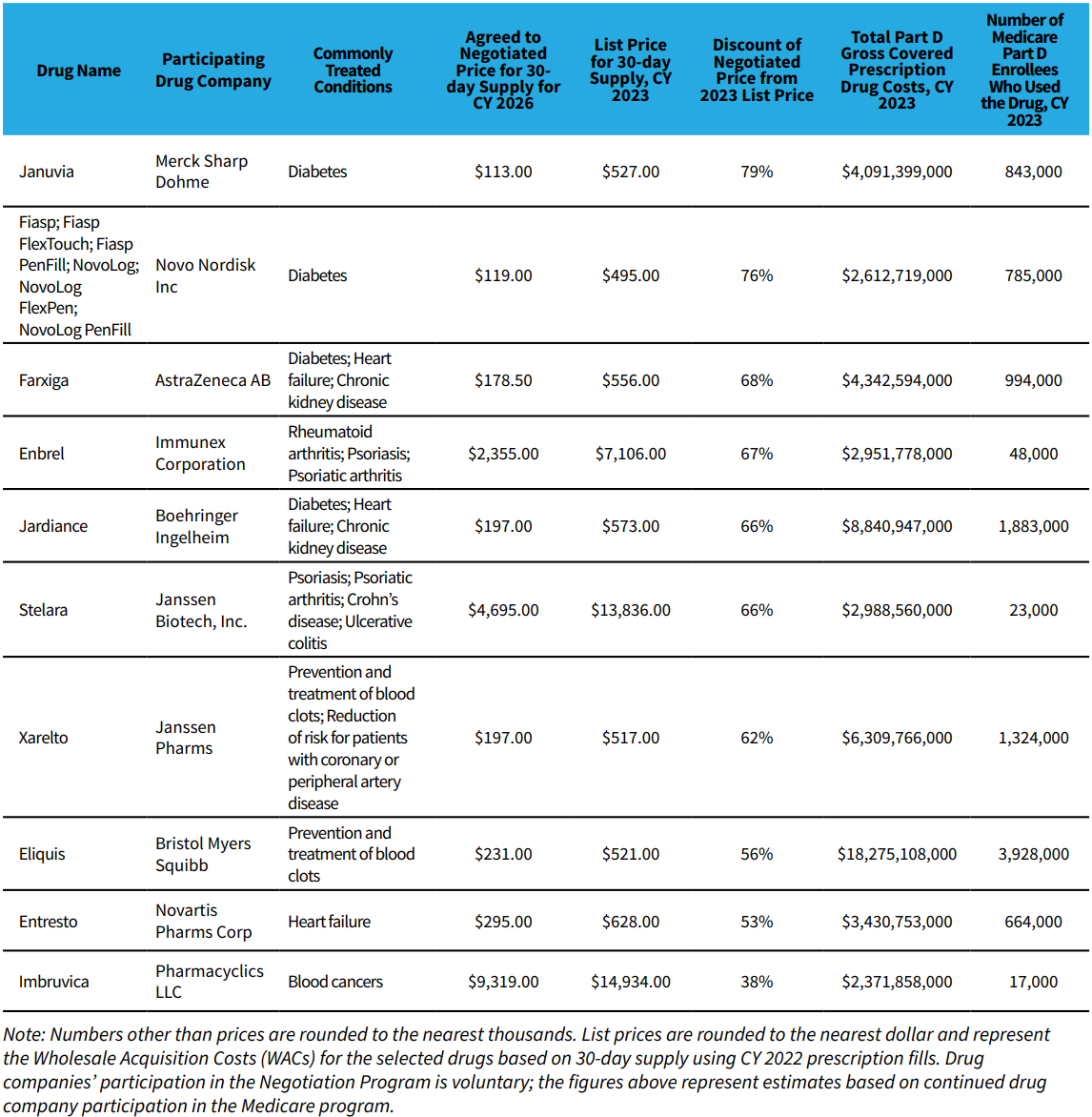

On August 15th, nearly two years to the day of when the Inflation Reduction Act (IRA) was signed into law, HHS published the results of the drug price negotiations, one of the major pillars of the legislation that impacts pharma manufacturers. Based on the data provided by HHS, the negotiated prices for the first 10 drugs selected resulted in discounts ranging between 38% and 79%, which would have saved an estimated $6B based on 2023 spend.

While this is being touted as a big win for the government and patients, I wanted to add some additional context. Based on my own experiences on both the manufacturer side as well as the consulting side, I am aware of many Medicare Part D drugs that currently discount at these levels. I’ve personally signed rebate contracts promising discounts from the high 20's to the mid 60's. While that’s a large range, rebates heavily depend on the drug, the company's portfolio and the larger competitive landscape. Taking these elements into account, here are my initial thoughts about the negotiated rates.

Source: CMS

How much of a discount did CMS actually negotiate? As individuals working in this industry know, most entities do not pay WAC for drugs, so CMS's comparison of the WAC price to the negotiated Part D price does not necessarily reflect the market price or accurate savings. To get a more precise picture of the negotiation impact, I calculated existing discounts for two of the products CMS negotiated using First Databank and publicly available data sources. Januvia already had a discount of at least 32% while Stelara had a discount of at least 39% off the CMS listed WAC prices. These estimates are just a starting point and it’s possible there are significant additional discounts in the form of existing rebates. When you take this into consideration, the 79% discount to Januvia and the 66% discount to Stelara start to look a little different.

How much did CMS leverage worldwide drug pricing versus existing US pricing? Often when we hear politicians discuss US drug pricing they compare it to the price of the same drug in other countries. Given this, I would guess CMS considered international drug pricing as a point of reference. Rest of world drug pricing varies heavily from country to country, so for this exercise I focused on Canadian pricing. Staying with the previous analogs, in Canada, Januvia costs roughly $120 and $130 while Stelara is somewhere between $5k and $6k. These numbers are within 10% of the negotiated rates published by CMS. While I don't think this was the sole data set used, it appears that CMS did reference it heavily in the negotiations.

How will the PBMs manage these negotiated drugs in their formularies? As noted above, I do not know how much of a rebate was being offered to Medicare Part D PBMs prior to the negotiation and I still need to do a bit more reading and research on who is retaining the negotiated rebates. With that being said, I cannot imagine that the manufacturers offering these discounts under Medicare Part D are going to pay additional rebates to the PBMs. I believe that these products may have been carved out of existing Medicare Part D rebate agreements. If that is the case, as we have seen from the reaction of PBMs to the phase-in criteria starting in 2025, they are not going to sit idly by and lose rebate revenue. How will they recoup the potential loss on these products as well as products to come? Will they expect additional rebates from other drugs in the class? Additional rebates for other drugs from these manufacturers?

There are many manufacturers whose drugs will not be up for negotiation in the next few years, and there are many more manufacturers whose drugs will never be negotiated under the current IRA guidance. Despite this, I believe all manufacturers will be impacted by the shifting landscape of the drug negotiations, whether they have a drug that is directly involved or not. Below are a couple of things that I will be keeping my eyes on in the upcoming contract negotiation cycle for Part D rebate agreements.

Did the cost of contracting in Medicare Part D just go up? There is one section of the Medicare Drug Price Negotiation Program Q&A on page 4 that makes me believe the cost of doing business with Medicare Part D PBMs just increased. CMS stated:

As required by law, Medicare prescription drug plans, including standalone Part D plans and Medicare Advantage-prescription drug plans, must include in their formularies the selected drugs for which CMS and the participating drug company have agreed to a negotiated August 2024 price. CMS will use its comprehensive formulary review process for Medicare prescription drug plans to assess any practices that may undermine access to selected drugs for people with Medicare.

I fully expect PBMs to continue to extract increased rebates from manufacturers across the board, and I do believe that they will do this through a variety of rebates and fees. Manufacturers have already seen an increase in the types of fees they pay. Gone are the days of a single administrative fee. That fee still exists but it is now augmented with Data fees, Enterprise fees, Compliance fees and the like. Will we start to see other fees based on the new CMS formulary review process?

Will Part D PBMs be willing to shift formularies for other drugs? On a positive note, if a manufacturer is willing to pay higher rebates, will the PBMs be willing to actually provide favorable formulary treatment for the drug? While I do believe PBMs will find new ways to replace rebate revenue, they may also begin to offer additional services and benefits for those fees. With continued guidance and focus on bona fide service fees and fair market value assessments, they have to continue to find value. Does this mean that an increased rebate may actually remove utilization management or keep a patient away from coinsurance?

There is a lot of formulary data that I plan to monitor over the next few months for indications of any changes coming into January 2025 and beyond. Stay tuned for additional assessments and thoughts around the IRA negotiations. If you have any questions or would like to discuss any of this live, please reach out.

Recent Articles

Physician Fee Schedule FAQ and Templates

CMS published its FAQ on Bona Fide Service Fee Certifications and ASP Reasonable Assumptions.

2026 GP Calendar

Key Government Pricing dates for 2026 to add to your Outlook or Google Calendar.

MDRP 2025 Wrap-up

Salient topics and key takeaways from the MDRP 2025 conference.

View All News & Opinions

Talk to an Expert

Get Started%20(1).avif)

.avif)