1/2/2024

The March 1, 2024 manufacturer deadline to enter into the Medicare Part D Discount Program agreement for 2025 is approaching. As manufacturers prepare their long-term forecasts for Medicare Part D financial liabilities, a key consideration is whether they qualify for the phase-in of applicable discounts under the Inflation Reduction Act. Let's review the various rebate rates that would apply in various scenarios, and then discuss the phase-in qualification requirements.

Base Scenario

Manufacturers who do not qualify for the discount phase-in pay the following rebates to plan sponsors for applicable drugs:

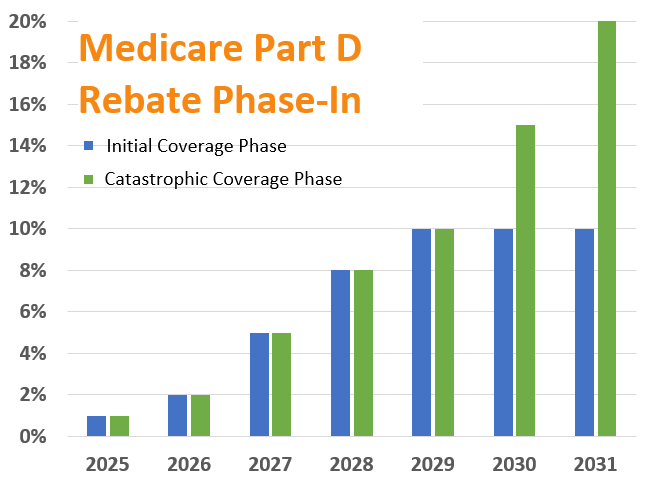

Reduced Discounts During the Phase-In

The IRA provides for lower discounts for:

- Specified Manufacturers' applicable drugs marketed as of August 16, 2022, and dispensed to beneficiaries eligible for the Low-Income Subsidy or LIS (see this CMS memo for LIS beneficiary income and resource limits).

- Specified Small Manufacturers' drugs marketed as of August 16, 2022, regardless of whether dispensed under the Low-Income Subsidy or not. Specified Small Manufacturers thus get lower rebate rates for a larger population of beneficiaries.

The schedule of rebate percentages is the same in both cases:

Specified Manufacturer

"Specified Manufacturer" is defined in section 1860D-14C(g)(4)(B)(ii) of the IRA as a manufacturer that meets the following criteria:

- Had a Coverage Gap Discount Program agreement in effect in 2021.

- Had total expenditures for all of its specified drugs covered by the CGDP agreements and under Part D for 2021 representing less than 1% of total expenditures for all Part D drugs in 2021.

- Had total expenditures for all of its specified drugs that are single source drugs and biological products for which payment may be made under Part B in 2021 representing less than 1% of the total expenditures under Part B for all drugs or biological products in 2021.

This definition requires aggregation of Medicare expenditures across all relevant manufacturer products, which is why CMS requires manufacturers to submit ownership information via HPMS. Per IRA:

[...] all entities, including corporations, partnerships, proprietorships, and other entities treated as a single employer under subsection (a) or (b) of section 52 of the Internal Revenue Code of 1986 are treated as one manufacturer.

CMS issued a detailed Methodology Memo for Identifying Specified Manufacturers and Specified Small Manufacturers. Note that the aggregation is not labeler code-driven, unlike some other government program requirements. CMS specifically called out that:

Because we do not currently prohibit a participating manufacturer from covering by its Discount Program agreement labeler code(s) assigned by the FDA to another manufacturer, the manufacturer must determine which labeler codes under each P number are attributable to the same manufacturer, and also determine if there are any labeler codes under different P numbers which also are attributable to the same manufacturer. To apply the aggregation rule, CMS will evaluate the ownership information submitted by manufacturers and determine which labeler codes, including, if any, labeler codes listed under different P numbers, must be attributed to and aggregated under the same manufacturer.

Specified Small Manufacturer

"Specified Small Manufacturer" is defined in section 1860D-14C(g)(4)(C)(ii) of the IRA as a manufacturer that meets the following criteria:

- Meets the "Specified Manufacturer" definition above.

- Had total expenditures under Part D for any one of its specified small manufacturer drugs covered by the CGDP agreements and under Part D in 2021 representing more than or equal to 80% of the total expenditures for all its specified small manufacturer drugs covered under Part D in 2021.

Essentially, this is a Specified Manufacturer whose business is dominated by a single drug. A "single drug" in this context has a broader definition than, say, an NDC-9. Per CMS:

In order to determine one drug’s share of a manufacturer’s Part D total expenditures, which we will use to identify specified small manufacturers, we first note that for drug products, one specified small manufacturer drug will include all dosage forms and strengths of a drug with the same active moiety and the same holder of the New Drug Application (NDA), inclusive of products that are marketed pursuant to different NDAs. For biological products, one specified small manufacturer drug will include all dosage forms and strengths of the biological product with the same active ingredient and the same holder of the Biologic Licensing Application (BLA), inclusive of products that are marketed pursuant to different BLAs. CMS will identify the holder of the NDA/BLA for a drug or biological product as reported in Drugs@FDA or FDA Purple Book.

The Methodology Memo linked above has additional details regarding drugs with combinations of ingredients, authorized generics, repackaged drugs, etc.

Do reach out to our team via the form below if you are working on assessing the impact of the Medicare Part D changes on your rebate liabilities, or with any other contracting or operational questions.

Recent Articles

Physician Fee Schedule FAQ and Templates

CMS published its FAQ on Bona Fide Service Fee Certifications and ASP Reasonable Assumptions.

2026 GP Calendar

Key Government Pricing dates for 2026 to add to your Outlook or Google Calendar.

MDRP 2025 Wrap-up

Salient topics and key takeaways from the MDRP 2025 conference.

View All News & Opinions

Talk to an Expert

Get Started%20(1).avif)

.avif)